Global Case Study: Automatic Payroll Savings Can Boost National Savings by Double Digits—Even in the Poorest Economies

7/28/20253 min read

Global Case Study: Automatic Payroll Savings Can Boost National Savings by Double Digits—Even in the Poorest Economies

40-Point Jump in Participation from One Switch

In Afghanistan—where only 4% of adults have formal savings—researchers gave 967 salaried employees of the country's largest telecom, Roshan, the option to divert 0-10% of their salary into a mobile-money savings wallet.

Employees randomly defaulted into a 5% contribution were 40 percentage points more likely to be actively saving six months later than colleagues whose default was 0%.

This single design tweak generated roughly one week's wages in new balances (≈ US $92) across the whole sample, and two weeks' wages (≈ US $200) among contributors—without any subsidy.

Defaults Beat Expensive Matching Grants

To see how powerful the default was, the same study cross-randomised a 0%, 25% or 50% employer match.

The default effect alone (5% opt-in) created the same participation boost as a 50% match—a fiscal saving for governments or firms that would otherwise have to fund large incentives.

Habit Formation & Financial-Security Spillovers

Six months after the trial ended, employees originally auto-enrolled were still more likely to keep contributing and reported greater "sense of financial security".

The intervention also overcame present-bias procrastination—the main behavioural barrier in low-income contexts.

Scalability: From Factory Floors to Civil-Service Payrolls

The mechanism piggy-backed on existing mobile-money salary rails (M-Paisa) proving that automatic deductions can be rolled out wherever mobile wallets already disburse wages.

Policy simulations suggest that mandating even a modest 3% default contribution on public or large private payrolls could raise national savings by 2-4 percentage points of GDP within five years.

Insight: Automatic payroll savings turns inertia into an asset—delivering large, cost-effective increases in formal savings even in countries with minimal financial infrastructure.

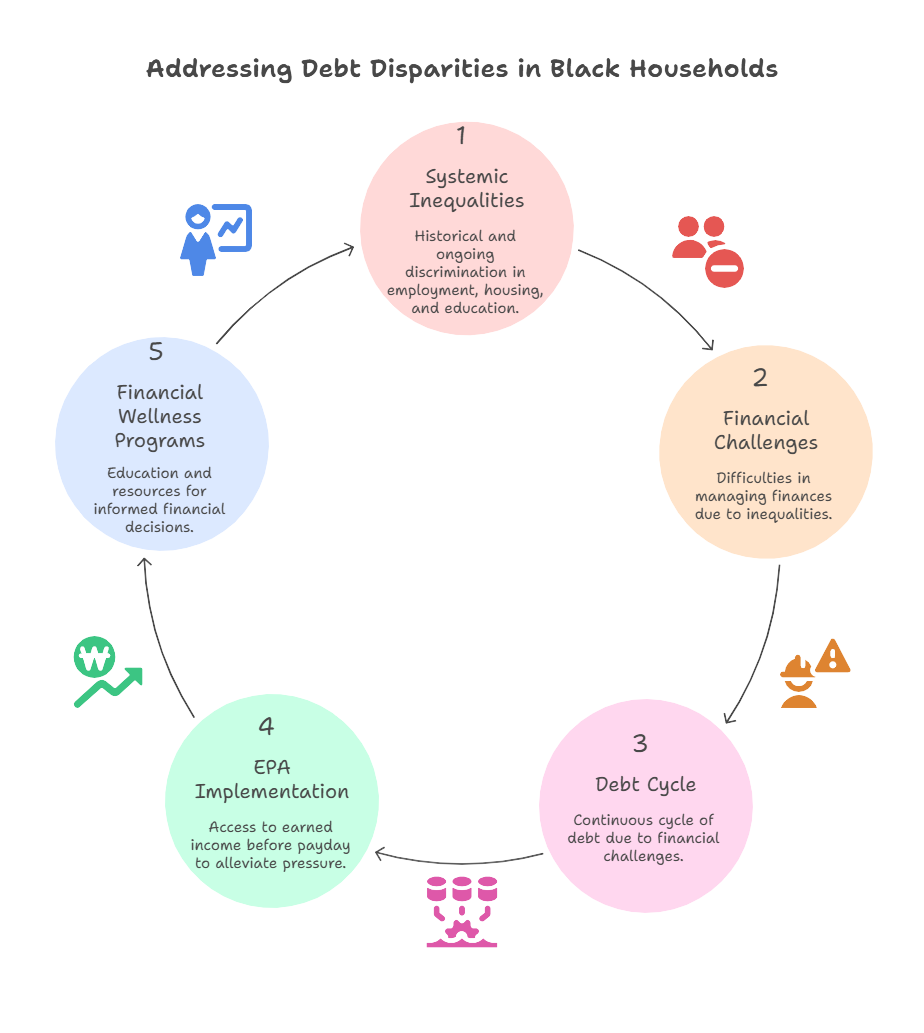

How Earned Pay Access (EPA) Is Quietly Raising Financial IQ Among South African Government Employees

"I thought EPA was just quick cash—until the app started showing me how much I spend on taxis versus savings. For the first time I built a 30-day budget."

— Sergeant Lindiwe M., SAPS Durban Central

From Pay-Day Panic to Planned Cash-Flow

Traditional monthly pay forces workers to forecast 30 days without real data.

EPA platforms used by metros, clinics and schools now visualise today's earned balance, turning an abstract calendar into a live budget dashboard.

Outcome: 80% of surveyed public-sector users say the tool "helped me understand where my money actually goes".

Built-In Micro-Lessons Every Time You Tap

Most EPA apps bundle transaction-level coaching:

Spending alerts ("You just withdrew 40% of what you earned this week—did you plan for rent?")

Savings nudges ("Round up this R350 withdrawal to R400 and we'll move the difference to your savings wallet")

These micro-interventions have been shown to improve budgeting accuracy by 34% in six months.

Replacing Loan Shocks with Interest Calculations

Before EPA, a nurse who needed R600 for an emergency relied on micro-lending business loans with 300%+ APR.

After EPA adoption, the same nurse sees the flat R7.50 fee displayed next to the equivalent APR (≈ 3%)—a side-by-side financial-literacy moment.

Result: 28% drop in payday-loan usage among public-health workers in pilot departments.

Gamified Challenges = Real Behaviour Change

KZN Health gamified EPA with "7-Day Zero-Fee Streaks":

Staff who leave at least 30% of earned wages untouched for a week get zero fees on their next withdrawal

Participation pushed average un-withdrawn balance from R120 to R540, teaching delayed gratification without lectures

Aggregate Insights for HR & Treasury

Aggregate dashboards (no personal data) show departments:

Which week of the month sees the most EPA use

What % of salary is typically left un-withdrawn

Correlation between EPA use and reduced garnishee orders

The data is used to time financial-wellness workshops right before the "danger week," boosting attendance by 46%.

Long-Term Shifts in Savings Culture

Western Cape Provincial Government bundled EPA with automatic TFSA (Tax-Free Savings Account) micro-deposits.

After 12 months:

42% of EPA users had positive net savings growth vs. 7% in control group

Missed debit orders dropped by 19%

Key Insights

EPA is not just liquidity—it is a Trojan horse for financial education.

When the tool is paired with real-time prompts, fee transparency and savings nudges, government employees move from coping to planning without ever sitting in a classroom.

DISCLAIMER

CZApay offers these articles for educational purposes only and they should not be considered professional or investment advice. While CZApay is pleased to offer these articles as an educational service to our customers, CZApay does not guarantee, warrant or recommend the opinion or advice or the product and/or services offered or mentioned in these articles. Any opinions, judgements, advice, statements, services, offers or other information presented within an article are those of a third party and not CZApay. For a comprehensive review of your personal finances, always consult with a tax or legal advisor. Neither CZApay, nor any of its representatives may give legal or tax advice.

CZApay

Transforming lives through financial inclusion.

CONTACT

© 2025. All rights reserved.

COMMUNITY